Crypto exchanges and their competitors are racing to adopt, -and ultimately democratize- financial services known from legacy finance. The three low hanging fruits are (1) interest accounts, (2) payments, and (3) tax services. Because of the low switching cost for customers, this transformation into crypto-banks will happen much faster than expected, leaving exchanges that don’t follow suit in the dust.

Other than the native assets of public blockchains, the most significant winners in the crypto space to date have been exchanges: Coinbase, Binance, Liquid Global, BitMEX, and Kraken are either confirmed or rumored to be worth more than $1 billion. Binance was even the fastest company in history to reach the coveted “unicorn” status.

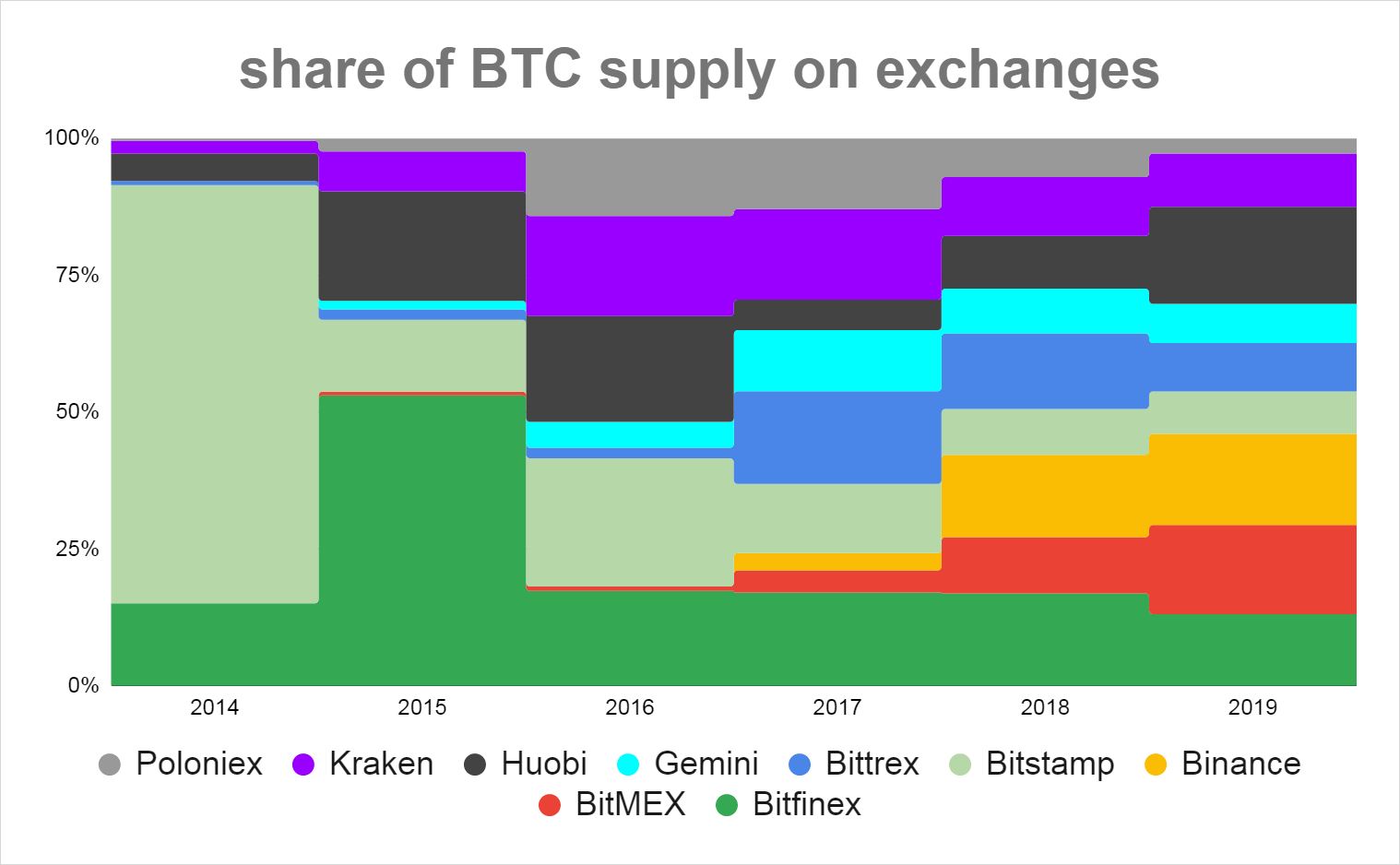

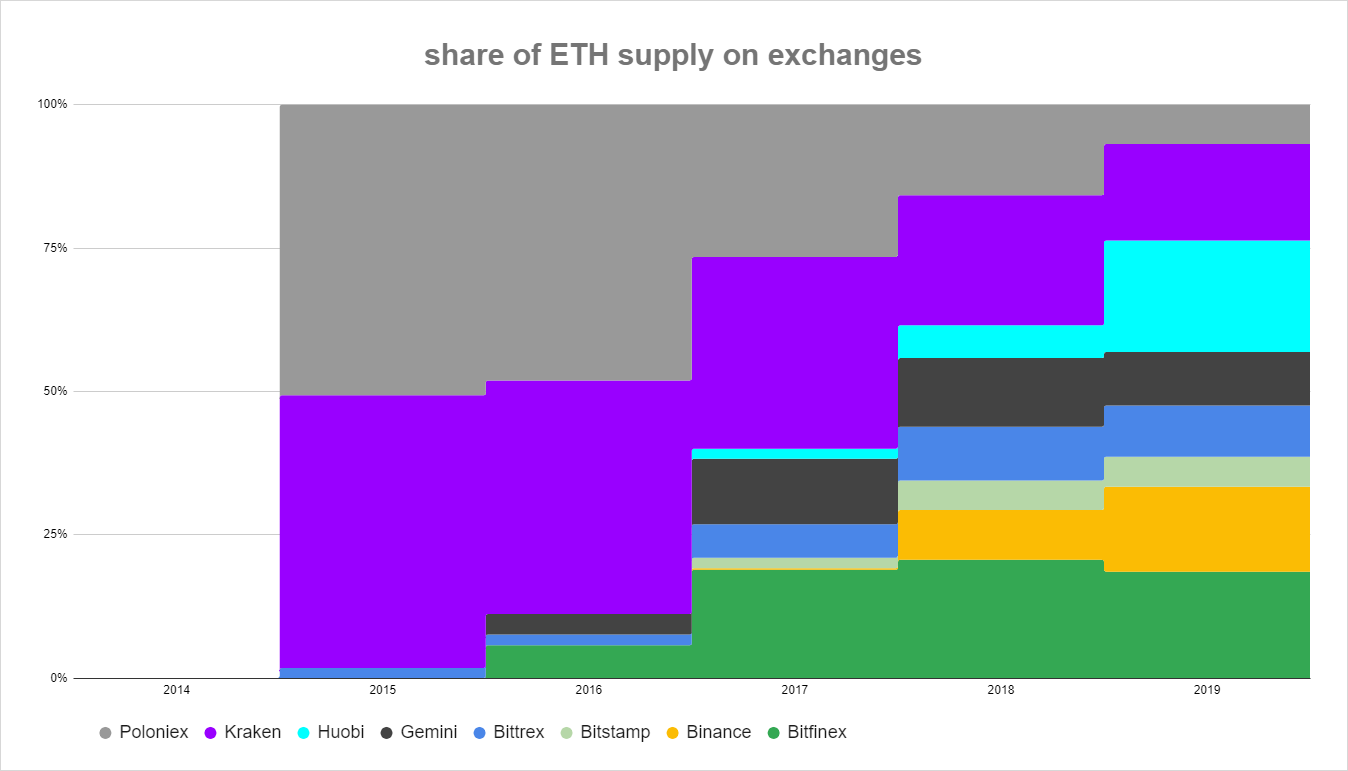

While valuations soar, crypto is an exceptionally dangerous industry for incumbents to rest on their laurels. The market leader in terms of spot exchange volume has shifted several times since 2016. Deposits of BTC & ETH in exchange custody paint a similar picture:

Crypto held on select exchanges as a proxy for exchange dominance. Source: CoinMetrics Network Data Pro

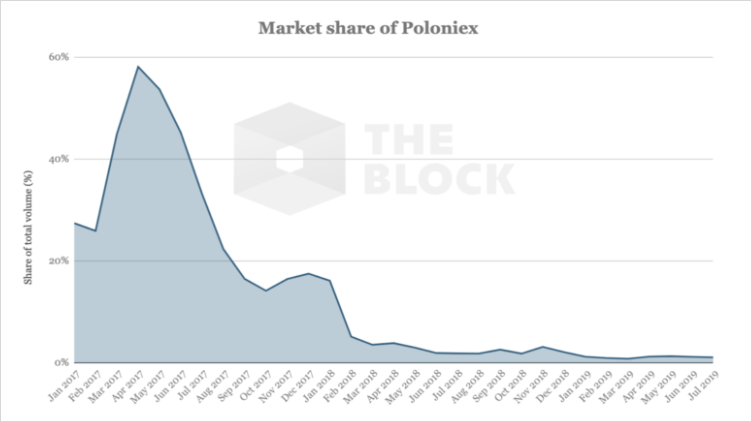

Poloniex is a particularly daunting example. Without any large shocks like an exchange hack or regulatory shakedown, it crashed from almost 60% market share in early 2017 to a meager 1% in May 2018, where it finally consolidated.

Poloniex share of total trading volume (incl. altcoins). Source: The Block

The volatile ups and downs can be explained by two factors:

- Network effect: Liquidity begets liquidity, on the way up and down. The marginal user is most likely to join the already largest exchange for a particular asset or service because it can offer the deepest markets and lowest spread, but leave as others are leaving.

- Low switching costs: If users dislike the service offered by one exchange, they can withdraw their assets and move to a different provider within minutes thanks to the permissionless payment rails provided by public blockchains. No paperwork required.

As a result of high user mobility, there’s a much faster feedback loop for the business decisions that exchanges make. If one exchange offers a new feature, others need to provide the same within a short period or risk falling behind. Crypto companies, in general, are among the fastest innovating in history due to the unique mix of a dynamic market, regulatory arbitrage, and a purely digital offering.

While this is great for customers, it puts a lot of pressure on exchanges to stay ahead of their peers. In this analysis, we will look at the features that we predict will be a standard offering for every spot exchange within the next two years.

(1) Interest accounts

As the crypto asset space consolidates fewer investable assets, it makes sense for exchanges to start optimizing for AUM and monetize via additional services instead of trading volume. Interest accounts, where the exchange matches borrowers and lenders for a small commission, replicate the original business model of an investment bank.

In a time of increasingly zero- or even negative interest rates in fiat currencies, crypto interest accounts can be a gateway technology to retain existing users and attract new users. We predict that yield comes primarily from three sources: staking, lending in exchange-internal money markets (e.g., to margin traders and market makers), and exchange external-lending and liquidity provision (e.g. in DeFi).

1.1 Staking-as-a-service

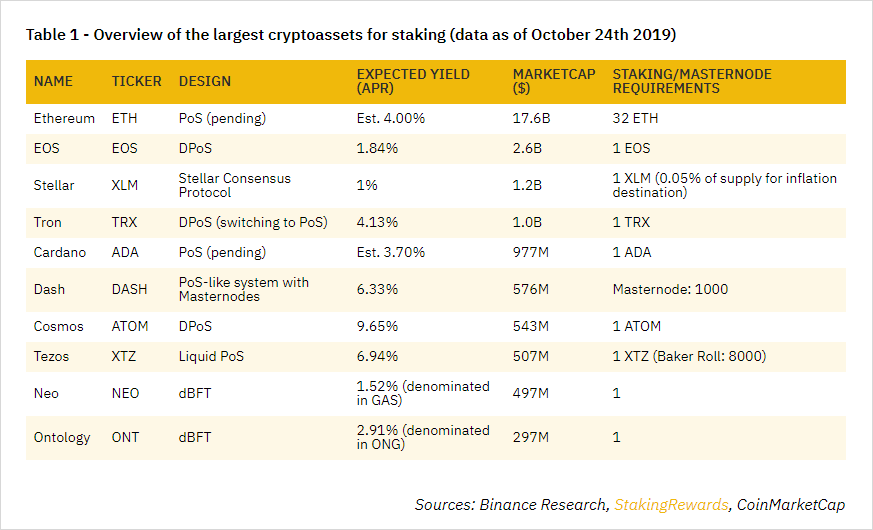

Most of the recently launched networks like Cosmos, Tezos, and Algorand, as well as upcoming networks like DFinity, Polkadot, NEAR, and Ethereum 2.0, use Proof-of-Stake as their Sybil-resistance mechanism of choice. In PoS, holders of the cryptocurrency can participate in the consensus process by staking their tokens.

If users already hold their tokens on an exchange, they might as well stake them to earn a little extra return. As a result, it makes little sense for an exchange to list a PoS token without offering a native staking service. In the case of Tezos, Coinbase, Binance, and Kraken have all rolled out staking within the span of one month.

Source: The Rise of Staking by Binance Research

1.2 Internal markets

The most natural kind of lending market exists between users of a given exchange, without funds ever leaving cold storage. There are two major sources of demand to borrow tokens: margin traders and market makers.

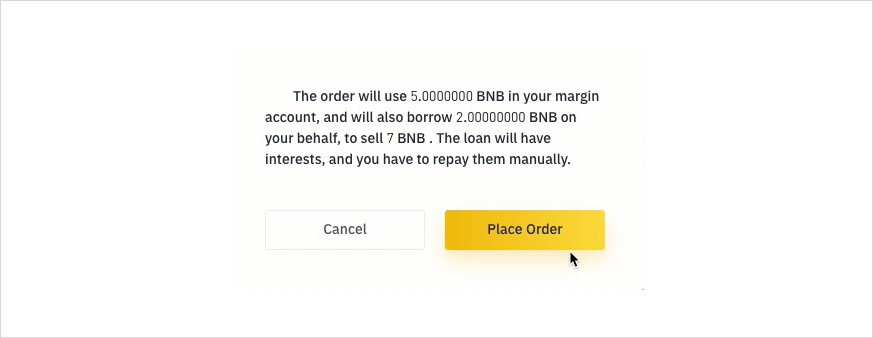

The biggest structural demand for borrowing comes from margin traders. On Bitfinex, Huobi, OKEx, and Binance traders need to borrow funds and deposit them into the margin wallet. They can then use these funds to trade the same book as spot traders. This is in contrast to derivatives exchanges like BitMEX or Deribit, where users merely trade financial contracts.

So structural borrowers for cryptos are short-sellers, whereas structural borrowers for USD and stablecoins are people who want to buy with leverage.

A margin-trader on Binance automatically taps into the BNB lending pool, paying interest to BNB savers. Source: Binance Margin Trading Guide

A smaller source of demand for borrowing comes from market-makers, who want to keep a small balance sheet and hence borrow cryptos with USD or USDT.

1.3. External markets

Apart from participating in an exchange-internal lending market, additional investment opportunities are available for users who are willing to withdraw their funds and experiment with different counterparties or even DeFi protocols.

Exchanges don’t want their customers to withdraw their funds and chase yield on their own, so they will start acting as a primer broker instead. The benefits of this are manifold:

- There are economies of scale, e.g., a Binance Broker could offer users a lower fee-tier on another exchange.

- The exchange has a more holistic view of a user’s risk profile, leading to lower capital requirements.

- It’s possible to trade on different venues without ever moving funds out of Coinbase Vault.

The other large benefit is that a primer broker can offer different interest accounts that are otherwise only available outside a user’s main exchange.

A prime example is synthetic USD accounts. On BitMEX and Deribit, the user can deposit BTC (and ETH in the case of Deribit) and sell the same amount of financial contracts. This creates a situation where he is long the underlying, e.g., 1 BTC, and short the financial, e.g., 1 BTC in futures contracts.

The reason investors can use derivatives to generate interest is the funding rate. Since perpetual swaps (by definition) never expire, there’s no natural price anchor for them to track the price of the underlying asset. To mitigate this issue, BitMEX developed the idea of a funding rate that is paid between longs and shorts every 8 hours. Due to the bullish bias of crypto markets, historically longs have paid shorts around 6% p.a. in funding.

As a result, investors can get paid to deposit BTC or ETH as collateral and short it, creating a high-yielding synthetic USD account. Arthur Hayes has explained this trade in a separate blog post.

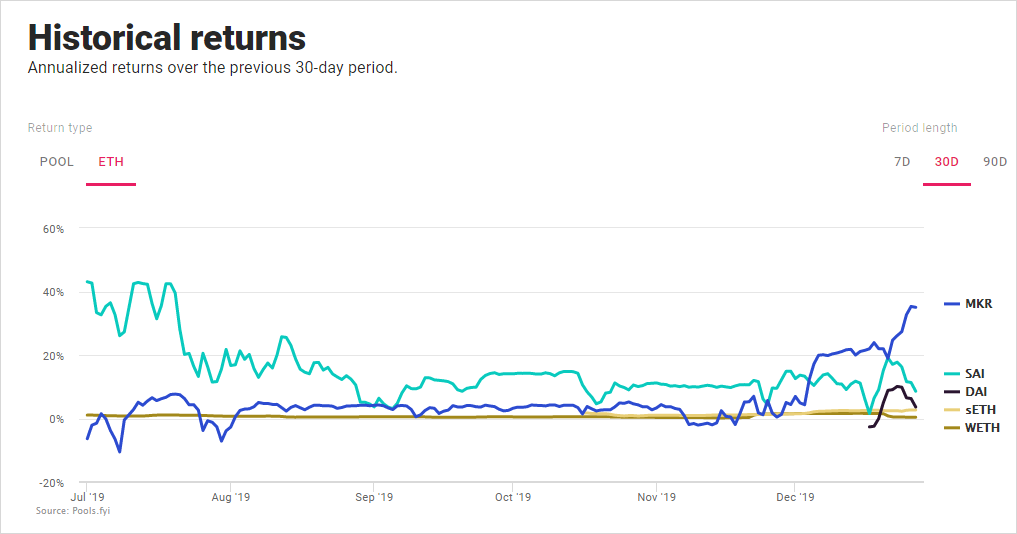

Exchanges can also tap into DeFi protocols like Maker, Compound, Kyber, DYDX, or Uniswap on behalf of their users. The first such example is OKEx, which just introduced support for the Dai Savings Rate.

There is no reason that users shouldn’t be able to deploy their assets with the click of a button on Compound or Uniswap.

Recent return history of various ETH pairs on Uniswap. Source: Link

Exchanges with their own prime brokers can offer their clients all of the earning opportunities in the crypto space from the comfort of their familiar interface, without any complicated on-chain transactions and self-custody.

(2) Payments

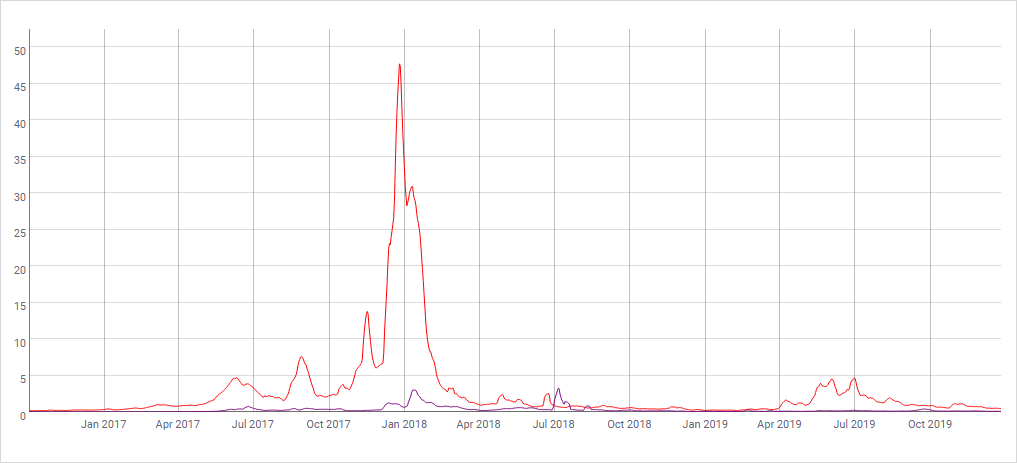

As our understanding of blockchains improves, it’s becoming more and more clear that they need high fees to be secure. Even though fees have been consistently low since the big spike 2017/18, it would be wise for exchanges to plan for a time when using the base layers of Bitcoin and Ethereum becomes once again costly.

Average USD transaction fees in Bitcoin (red) and Ethereum (purple). Source: CoinMetrics.io

Exchanges will develop payment networks that span both other exchanges as well as merchants for users to transact with. Performing smaller payments between relatively trusted parties on secondary private ledgers makes sense for several reasons.

- These transactions don’t benefit from the assurances of public blockchains, and may not be willing to pay a high fee.

- a private ledger can handle transactions faster and more privately than a public one.

- Easier to offer good UX with account recovery options and transfer to human-readable account names like email addresses instead of public key hashes.

2.1 Exchange <> Exchange

Several crypto firms dream of becoming the “DTCC of Bitcoin.” Among those that offer clearing and settlement services for institutions are BitGo and the Liquidity Offset Network, a joint venture between Circle, Coinbase, Galaxy Digital, Bakkt, and others.

The unwillingness to join the financial stack of a competitor could benefit more “neutral” solutions like Blockstream’s Liquid, which are basically MultiSig wallets between large exchanges. While Liquid hasn’t seen any real adoption to date, we find it likely that will change the moment fees spike up.

Federated sidechains like Liquid could see an influx of new users if fees on the base layer become prohibitive. Source: Liquid

Then exchanges can allow users to exchange quickly and privately, to the benefit of users who are annoyed by slow transactions and high fees of the blockchain base layers.

2.2 Customer <> Merchant

Exchanges will make it easier to receive crypto as a merchant as well as to spend crypto as a user.

Merchants are natural sellers of crypto, so it would make sense for exchanges to handle their payments directly. This is another example where Coinbase has been leading the market in terms of vertical integration with its Commerce product.

On the user side, it seems the concept of crypto-backed Visa and Mastercards, which largely stayed behind expectations in 2017–2018 for regulatory reasons, could finally take off. There are already Coinbase Card and Crypto.com (US + SG only), with Binance launching a card specifically for travelers. These cards serve the double-purpose of allowing users to more easily spend their crypto, as well as sourcing trading volume for crypto/fiat pairs to the exchanges themselves.

Source: Crypto.com

Another example is Bitrefill (a crypto-only gift card store) integrating with Bitfinex.

(3) Tax services

A topic that has received surprisingly little attention to date is tax services. We think that exchanges should invest a lot more into this area for two reasons:

- Exchanges and their users are completely aligned in their interest in preventing money from flowing out of the crypto space to the taxman via tax-loss harvesting and liquidity management.

- Uncertainty over taxes and how to calculate them increases both the mental and financial cost of holding and spending cryptocurrency.

3.1 The value of education

Given the novelty of the topic, most tax attorneys and financial advisors are inexperienced when dealing with clients who have crypto taxes to declare. Hence it is important that users educate themselves on the process, so they can more easily calculate their own taxes and prevent costly mistakes. To help with that, Coinbase has created a tax guide for its US users.

3.2 Easy integration with tax services

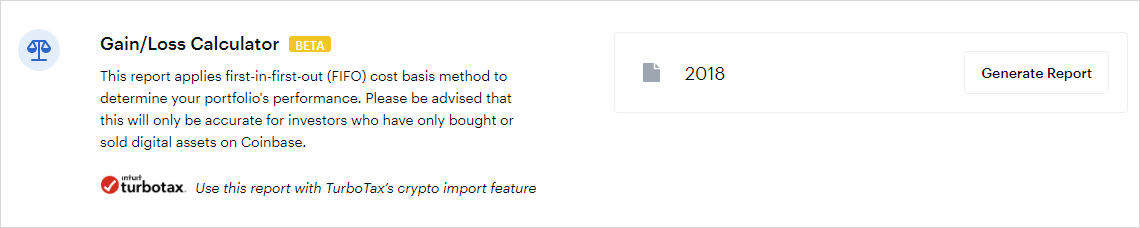

Exchanges can do a better job of helping users with their taxes at year-end. The prerequisite for any kind of tax advice is that the exchange needs a holistic view of their customers’ crypto portfolios and trading records.

Every exchange has native access to the asset and trading data from their venue, but for users who trade on several venues, there needs to be a way to either important external data (e.g., via information-sharing agreements) or easily export data into a third-party tax program like TurboTax, CoinTracker, ZenLedger, or CoinTracking.

A native Gain/Loss tracker for investors who use Coinbase exclusively, eliminating the need for any third-party tax programs. Source: Coinbase

3.3 Tracking tax events

The biggest hurdle to spending crypto today is not necessarily a lack of acceptance or expectations of future gains. It is that every single payment triggers a tax event. While orgs like CoinCenter work towards easing that burden from the regulatory side, crypto banks can do their part by logging all the trades.

3.4 Tax-loss harvesting

When users have incurred a tax-relevant loss on a crypto asset, they can realize that loss to offset taxes on gains or income elsewhere. If applied correctly, the resulting tax bill would be lower. Shortly before we published this article, Kraken actually sent an explainer on tax-loss harvesting to their users.

3.5 Liquidity management

An important part of investing is correctly managing one’s liquidity needs. Whenever users are forced to liquidate an asset for liquidity or tax reasons, they tend to get a much worse price than they otherwise would.

Imagine an investor has held 1 BTC for eleven months. If he could hold it one more month before selling, the asset becomes long-term as opposed to short-term, leading to a more favorable tax rate. But by selling that asset right now, he ends up losing out on that tax benefit.

In cases like these, exchanges can offer emergency liquidity in the form of crypto-collateralized loans. Similar to margin-trading, the user can borrow fiat against his crypto on the exchange to pay his expenses without creating a tax event from selling his crypto.

(4) Where is the competition?

Crypto exchanges are not the only companies in this space who are racing toward the coveted goal of becoming full-stack financial service providers. In fact, custodians and wallets also push into the financial services space, incl. B&L (borrowing and lending).

Source: It’s a Mad Mad Mad Mad World (1963).

BitGo Prime, for example, offers borrowing and lending, while OSL custody (a leading Asian custodian) offers time deposits (meaning they borrow money from customers for a fixed time period). Blockchain.com has its own B&L desk for institutional customers. It’s only a matter of time before they roll these products out to their retail customers.

Meanwhile, Crypto.com approaches the market from the opposite angle. Starting as a wallet, they first added B&L, and finally an exchange. While competition from non-exchange players has been relatively tame, we expect it to heat up with the entrance of new players like Matrixport and Babel Finance in Asia, as well as BlockFi in the US.

At the end of the day, BTC and ETH are just capital, and companies compete to consolidate as much of it as possible. With capital come financial services, and the opportunity to generate more capital.

Conclusion

Over the next years, competition between crypto exchanges, wallets, and custodians will shift from horizontal expansion (more and more assets) to vertical integration (allowing users to do more with my existing assets.) While coming from different directions, they all share the same goal of becoming a crypto bank. Their leading indicator of success will be AUM, which they monetize via financial services. In the process, these financial services will become more widely accessible and cheaper than ever before.

AUTHOR(S)

Crypto researcher writing w/@zhusu for @DeribitInsights and uncommoncore.co, podcast: uncommoncore.co/podcast/

THANKS TO

Thanks to Su Zhu, Mike Co, Tiantian Kullander, panek, and Dan Burke for their contributions